18.04.2024 / 10:00

Model Implementation - The Future of Internal Market Risk Models according to FRTB

Financial Markets

Have internal market risk models become obsolete after the "Fundamental Review of the Trading Book" (FRTB) regulations come into force? In the following, we will examine why many institutions are skeptical about model implementation in accordance with the FRTB and why it could nevertheless be useful. To this end, the aim is not only to achieve the fullest possible coverage of the usual cost and income variables in business case analyses but also to provide an overview of relevant "soft" aspects.

The regulatory changes with Basel II in the 1990s made the use of internal market risk models very attractive for many banks. As a result, almost all major banks in Germany have opted for and successfully implemented such models.

The financial crisis made it clear that banks need significantly more capital to remain viable and survive crisis scenarios. The regulatory requirements were raised accordingly:

With the changes to the minimum capital requirements ("Basel 2.5") published in 2009, previously unconsidered risk aspects were addressed through the introduction of stressed VaR and incremental risk charge. To be later followed by the introduction of lump-sum capital buffers (particularly for systemically important institutions) to strengthen the capital base across the board.

In addition, the pooling of banking supervision of the largest banks at the ECB in 2014 and the associated reform of supervisory practice led to a trend towards higher requirements for processes, systems, and documentation standards.

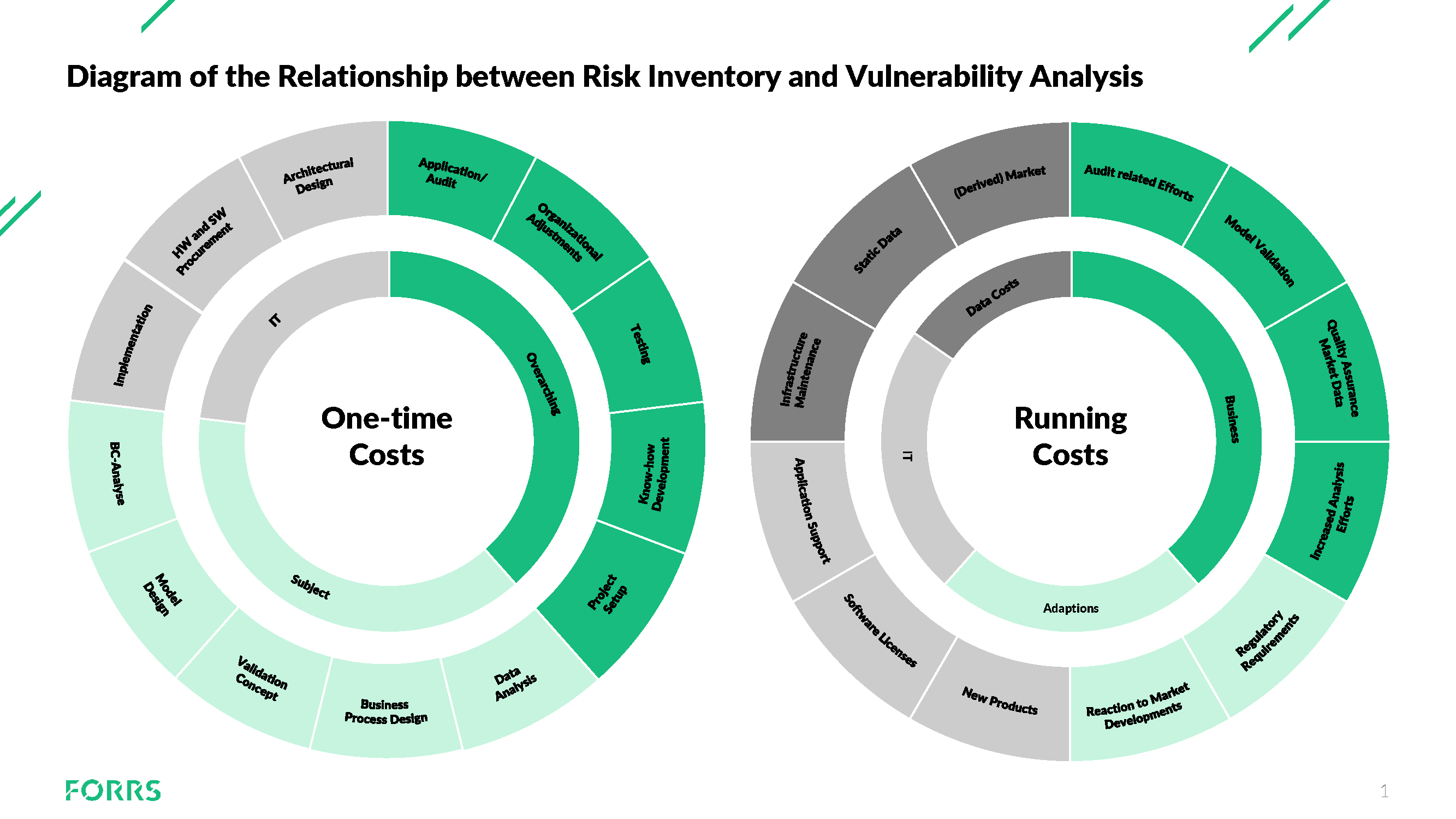

However, none of this has led to institutions fundamentally questioning the operation of internal market risk models. A look at the main drivers (Figure 1) for the "internal market risk model" business case for most banks reveals the causes:

Capital charge savings: The introduction of stressed VaR and the incremental risk charge has led to an increase in the risk-weighted assets based on internal models. However, the savings to be achieved remained at a high level (compared to the standardised approach based capital charge). In this context, the introduction of additional capital buffers (see above) even led to an increase in the attractiveness of internal market risk models, as the correspondingly lower RWAs with the same positioning make it easier to achieve higher ratios.

Implementation/project costs of the new metrics: The implementation costs of the new metrics to be implemented were certainly not negligible. However, the costs were rather small, especially compared to an entirely new implementation.

Running costs: Regarding running costs, the implementation of the necessary changes was accompanied by corresponding increases. However, these are not considered to be substantial either.

Long-term usability of the model/stability: The initial approval of an internal market risk model is often lengthy but, in any case, very time-consuming in many respects. In the past, however, it has been observed that once approval for internal models has been granted, it usually remains valid over a long period of time. Qualitative surcharge factors and surcharge factors based on backtesting results may cause the magnitudes of the capital savings to fluctuate, but it is very unlikely that the operating license for an internal market risk model will be withdrawn.

Figure 1: IIllustration of the relationship between risk inventory and vulnerability analysis.

Under the FRTB (valid from 2025), all previously applicable risk metrics will be replaced or redefined:

The expected shortfall will replace value-at-risk, while the liquidity of the risk factors will also be taken into account.

Additional capital is required for risk factors that are classified as "non-modellable" due to a lack of market observability.

In the future, equity exposures, government bonds, and loans that have already defaulted must be considered in the default risk.

FRTB also changes fundamental framework conditions such as the eligibility criteria (P&L attribution) or the distinction between banking and trading books. In addition to FRTB, the finalization of the Basel III rules introduced the so-called output floor, according to which the savings from internal models compared to standard approaches - across all risk types - can amount to a maximum of 27.5 percent. We analyze the impact of these drastic changes on the internal market risk model business case based on the criteria defined above:

Capital Savings

While significant increases in RWAs were feared on the basis of consultations and even after the first "final" publication of the new minimum capital requirements in January 2016, the assessment of any additional capital requirements after some recalibrations is rather moderate.

However, the impact of the output floor is very significant, particularly for major German banks with their predominantly credit-heavy business models. This means that if an internal model for an individual risk type with a comparatively high impact reduces the capital charge to such an extent that savings of more than 27.5% can be achieved for this risk type, other risk types can be "subsidized" as a result. Additional internal models for less significant risk types, therefore, become less attractive. For most major German banks, credit risk is by far the most critical risk type, so it is expected that this will be the focus of the further development of internal models.

Implementation Costs

The implementation costs for an internal market risk model by FRTB are immense: the first step is to develop a complex risk model for which no market standard has yet been established that could be used as a benchmark. This is followed by the implementation (including testing) of this model. Experience has shown that setting up the necessary operational processes, including documentation, registering the model with the supervisory authority, and the subsequent approval process, are very time-consuming in every respect. Of course, the model can only be used after approval by the supervisory authority.

Finally, it should be noted here that, in addition to the implementation of the internal model, the regulatory requirements additionally include the calculation of capital requirements in accordance with the standardised approach.

Running Costs of an Internal Model according to FRTB

The running costs of an internal market risk model by the FRTB are also expected to increase significantly compared to the status quo. The main reasons for this are increased infrastructure requirements due to the strong increase in the number of valuation processes required, the analysis costs associated with the greater complexity of the metrics, and the increased data requirements (e.g., high-quality market data time series covering a very long period or transaction data needed to derive the modelability of risk factors).

Long-term Usability of the Model/Stability

With FRTB, mere approval of the internal model by the supervisory authority is no longer sufficient to allow the model to operate. An additional criterion is the result of the P&L attribution exercise to be carried out on a desk-by-desk basis. If the limits defined in this context are exceeded, the determination of capital requirements for the portfolios concerned reverts to the standardised approach.

In summary, the hurdles for an FRTB based internal model approach are high, and the associated risks are enormous. Particularly in the current market environment (low volume in high-margin business segments, reduction in product complexity), many banks are therefore reluctant to invest in an internal market risk model in accordance with FRTB.

Nevertheless, there are some "soft" aspects that need to be weighed up before a decision is made against continuing to operate an internal model. These aspects are often difficult to quantify in monetary terms as part of a business case analysis but could have a huge impact, especially long term.

First and foremost, a possible loss of risk management quality should be mentioned here. The operation of an internal model presupposes that existing and potential market risk exposures are dealt with permanently and applying best practice. The operation of an internal model requires a high level of expertise in the organization's risk management and control units. This includes both an in-depth understanding of the products traded and the ability to operate and further develop the internal risk model. A well-positioned risk management system makes an extremely valuable contribution to minimizing unexpected losses. The reduction in personnel and expertise associated with a move away from internal models increases the corresponding risks.

Another aspect is that the implementation costs are heavily dependent on the complexity and liquidity of the portfolios. At the same time, the P&L attribution criterion is easier to achieve for clearly positioned portfolios than for well-hedged portfolios with residual risks. As FRTB allows a desk-specific decision "internal model vs. standard approach," corresponding mixed strategies can be promising.

In addition, the regulatory situation may well change: For example, the degree of effectiveness of the output floor could change due to changed framework conditions in other risk types or institution-specific shifts between risk types, thus favoring an internal market risk model.

It is also to be expected that the FRTB reforms affecting Pillar I will sooner or later become at least partially relevant for Pillar II. It is conceivable that a decision against an internal model, which is reasonable at first glance from today's perspective, will be put to the test again in the medium term due to these aspects. If the necessary expertise then must be built again, the costs will be much higher.

Conclusion

Operating an internal model by FRTB can significantly enhance or maintain an institution's reputation in the market. Due to these non-quantifiable aspects, it is advisable not to write off internal FRTB models prematurely. The decision for or against an internal market risk model in accordance with the FRTB is a complex one and should be made by each institution, considering all fundamentally relevant aspects as well as the individual strategic orientation.